Value creation has changed over time, however. Since 2020, the cost of debt has increased and liquidity in debt markets is harder to access given current interest rates, asset valuations, and typical bank borrowing standards. Fund performance has suffered as a result: PE buyout entry multiples declined from 11.9 to 11.0 times EBITDA through the first nine months of 2023.

Even as debt markets begin to bounce back, a new macroeconomic reality is setting in—one that requires more than just financial acumen to drive returns. Buyout managers now need to focus on operational value creation strategies for revenue growth, as well as margin expansion to offset compression of multiples and to deliver desired returns to investors.

Based on our years of research and experience working with a range of private-capital firms across the globe, we have identified two key principles to maximize operational value creation.

- First, buyout managers should invest with operational value creation at the forefront. This means that in addition to strategic diligence, they should conduct operational diligence for new assets. Their focus should be on developing a rigorous, bespoke, and integrated approach to assessing top-line and operational efficiency. During the underwriting process, managers can also identify actions that could expand and improve EBITDA margins and growth rates during the holding period, identify the costs involved in this transformation, and create rough timelines to track the assets’ performance. And if they acquire the asset, the manager should: 1) clearly establish the value creation objectives before deal signing, 2) emphasize operational and top-line improvements after closing, and 3) pursue continual improvements in ways of working with portfolio companies. Meanwhile, for existing assets, the manager should ensure that the level of oversight and monitoring is closely aligned with the health of each asset.

- Second, everyone should understand and have a hand in improving operations. Within the PE firm, the operating group and deal teams should work together to enable and hold portfolio companies accountable for the execution of the value creation plan. This begins with an explicit focus on “linking talent to value”—ensuring leaders with the right combination of skills and experience are in place and empowered to deliver the plan, improve internal processes, and build organizational capabilities.

In our experience, getting these two principles right can significantly improve PE fund performance. Our initial analysis of more than 100 PE funds with vintages after 2020 indicates that general partners that focus on creating value through asset operations achieve a higher internal rate of return—up to two to three percentage points higher, on average—compared with peers.

The case for operational efficiency

The ongoing macroeconomic uncertainty has made it difficult for buyout managers to achieve historical levels of returns in the PE buyout industry using old ways of value creation.2 And it’s not going to get any easier anytime soon, for two reasons.

Higher-for-longer rates will trigger financing issues.

The US Federal Reserve projects that the federal funds rate will remain around 4.5 percent through 2024, then potentially drop to about 3.0 percent by the end of 2026. Yet, even if rates decline by 200 basis points over the next two years, they will still be higher than they were over the past four years when PE buyout deals were underwritten.

This could create issues with recapitalization or floating interest rate resets for a portfolio company’s standing debt. Consider that the average borrower takes a leveraged loan at an interest coverage ratio of about three times EBIDTA (or 3x). With rising interest expenses and additional profitability headwinds, these coverage ratios could quickly fall below 2x and get close to or trip covenant triggers around 1x. In 2023, for example, the average leveraged loan in the healthcare and software industries was already at less than a 2x interest coverage ratio.5 To avoid a covenant breach, or (if needed) increasing recapitalization capital available without equity paydown, managers will need to rely on operational efficiency to increase EBITDA.

Valuations are mismatched.

If interest rates remain high, the most recent vintage of PE assets is likely to face valuation mismatches at exit, or extended hold periods until value can be realized. Moreover, valuation of PE assets has remained high relative to their public-market equivalents, partly a result of the natural lag in how these assets are marked to market. As the CEO of Harvard University’s endowment explained in Harvard’s 2023 annual report, it will likely take more time for private valuations to fully reflect market conditions due to the continued slowdown in exits and financing rounds.6

Adapting PE’s value creation approach

Operational efficiency isn’t a new concept in the PE world. We’ve previously written about the strategic shift among firms, increasingly notable since 2018, moving from the historical “buy smart and hold” approach to one of “acquire, align on strategy, and improve operating performance.”

However, the role of operations in creating more value is no longer just a source of competitive advantage but a competitive necessity for managers. Let’s take a closer look at the two principles that can create operational efficiency.

Invest with operational value creation at the forefront.

PE fund managers can improve the profitability and exit valuations of assets by having operations-related conversations up front.

Assessing new assets. Prior to acquiring an asset, PE managers typically conduct financial and strategic diligence to refine their understanding of a given market and the asset’s position in that market. They should also undertake operational diligence—if they are not already doing so—to develop a holistic view of the asset to inform their value creation agenda.

Operational diligence involves the detailed assessment of an asset’s operations, including identification of opportunities to improve margins or accelerate organic growth. A well-executed operational-diligence process can reveal or confirm which types of initiatives could generate top-line and efficiency-driven value, the estimated cash flow improvements these initiatives could generate, the approximate timing of any cash flow improvements, and the potential costs of such initiatives.

The results of an operational-diligence process can be advantageous in other ways, too. Managers can use the findings to create a compelling value creation plan, or a detailed memo summarizing the near-term improvement opportunities available in the current profit-and-loss statement, as well as potential opportunities for expansion into adjacencies or new markets. After this step is done, they should determine, in collaboration with their operating-group colleagues, whether they have the appropriate leaders in place to successfully implement the value creation plan.

These results can also help managers resolve any potential issues up front, prior to deal signing, which in turn could increase the likelihood of receiving investment committee approval for the acquisition. Managers also can share the diligence findings with co-investors and financiers to help boost their confidence in the investment and the associated value creation thesis.

It is crucial that managers have in-depth familiarity with company operations, since operational diligence is not just an analytical-sizing exercise. If they perform operational diligence well, they can ensure that the full value creation strategy and performance improvement opportunities are embedded in the annual operating plan and the longer-term three- to five-year plan of the portfolio company’s management team.

Assessing existing assets. When it comes to existing assets, a fundamental question for PE managers is how to continue to improve performance throughout the deal life cycle. Particularly in the current macroeconomic and geopolitical environment, where uncertainty reigns, managers should focus more—and more often—on directly monitoring assets and intervening when required. They can complement this monitoring with routine touchpoints with the CEO, CFO, and chief transformation officer (CTO) of individual assets to get updates on critical initiatives driving the value creation plan, along with ensuring their operating group has full access to each portfolio company’s financials. Few PE managers currently provide this level of transparency into their assets’ performance.

To effectively monitor existing assets, managers can use key performance indicators (KPIs) directly linked to the fund’s investment thesis. For instance, if the fund’s investment thesis is centered on the availability of inventory, they may rigorously track forecasts of supply and demand and order volumes. This way, they can identify and address issues with inventory early on. Some managers pull information directly from the enterprise resource planning systems in their portfolio companies to get full visibility into operations. Others have set up specific “transformation management offices” to support performance improvements in key assets and improve transparency on key initiatives.

We’ve seen managers adopt various approaches with assets that are on track to meet return hurdles. They have frequent discussions with the portfolio company’s management team, perform quarterly credit checks on key suppliers and customers to ensure stability of their extended operations, and do a detailed review of the portfolio company’s operations and financial performance two to three years into the hold period. Managers can therefore confirm whether the management team is delivering on their value creation plans and also identify any new opportunities associated with the well-performing assets.

If existing assets are underperforming or distressed, managers’ prompt interventions to improve operations in the near term, and improve revenue over the medium term, can determine whether they should continue to own the asset or reduce their equity position through a bankruptcy proceeding. One manager implemented a cash management program to monitor and improve the cash flow for an underperforming retail asset of a portfolio company. The approach helped the portfolio company overcome a peak cash flow crisis period, avoid tripping liquidity covenants in an asset-backed loan, and get the time needed for the asset’s long-term performance to improve.

Reassess internal operations and governance.

In addition to operational improvements, managers should also assess their own operations and consider shifting to an operating model that encourages increased engagement between their team and the portfolio companies. They should cultivate a stable of trusted, experienced executives within the operating group. They should empower these executives to be equal collaborators with the deal team in determining the value available in the asset to be underwritten, developing an appropriate value creation strategy, and overseeing performance of the portfolio company’s management.

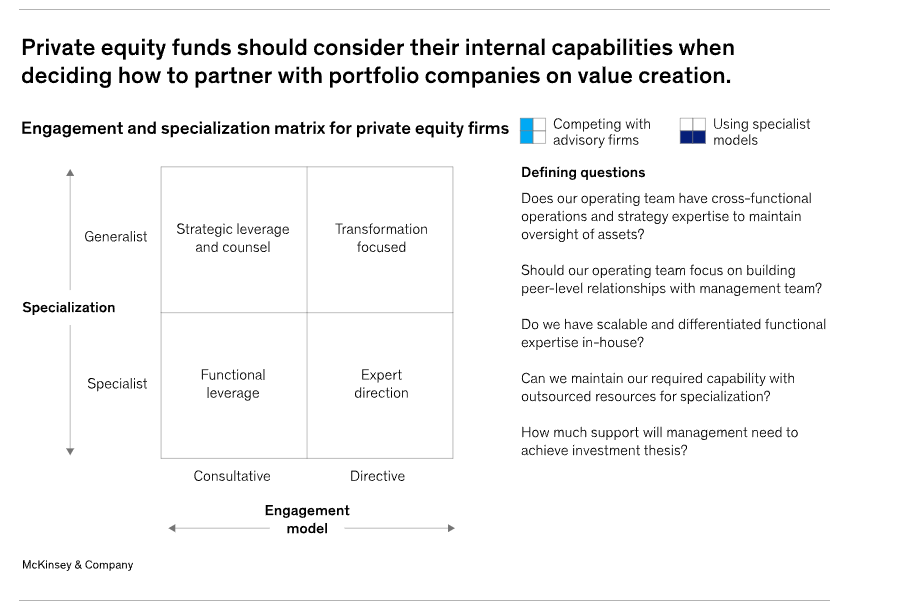

Shift to a ‘just right’ operating model for operating partners. The operating model through which buyout managers engage with portfolio companies should be “just right”—that is, aligned with the fund’s overall strategy, how the fund is structured, and who sets the strategic vision for each individual portfolio company.

There are two types of engagement operating models—consultative and directive. When choosing an operating model, firms should align their hiring and internal capabilities to support their operating norms, how they add value to their portfolio companies, and the desired relationship with the management team (exhibit).

Exhibit

Take the example of a traditional buyout manager that acquires good companies with good management teams. In such a case, the portfolio company’s management team is likely to already have a strategic vision for the asset. These managers may therefore choose a more consultative engagement approach (for instance, providing advice and support to the portfolio company for any board-related issues or other challenges).

For value- or operations-focused funds, the manager may have higher ownership in the strategic vision for the asset, so their initial goal should be to develop a management team that can deliver on a specific investment thesis. In this case, the support required by the portfolio company could be less specialized (for example, the manager helps in hiring the right talent for key functional areas), and more integrative, to ensure a successful end-to-end transformation for the asset. As such, a more directive or oversight-focused engagement operating model may be preferred.

Successful execution of these engagement models requires the operating group to have the right talent mix and experience levels. If the manager implements a “generalist” coverage model, for example, where the focus is on monitoring and overseeing portfolio companies, the operating group will need people with the ability (and experience) to support the management in end-to-end transformations. However, a different type of skill set is required if the manager chooses a “specialist” coverage model, where the focus is on providing functional guidance and expertise (leaving transformations to the portfolio company’s management teams). Larger and more mature operating groups frequently use a mix of both talent pools.

Empower the operating group. In the past, many buyout managers did not have operating teams, so they relied on the management teams in the portfolio companies to fully identify and implement the value creation plan while running the asset’s day-to-day operations. Over time, many top PE funds began to establish internal operating groups to provide strategic direction, coaching, and support to their portfolio companies. The operating groups, however, tended to take a back seat to deal teams, largely because legacy mindsets and governance structures placed responsibility for the performance of an asset on the deal team. In our view, while the deal team needs to remain responsible and accountable for the deal, certain tasks can be delegated to the operating group.

Some managers give their operating group members seats on portfolio company boards, hiring authority for key executives, and even decision-making rights on certain value creation strategies within the portfolio. For optimal performance, these operating groups should have leaders with prior C-suite responsibility or commensurate accountability within the PE fund and experience executing cross-functional mandates and company transformations. Certain funds with a core commitment to portfolio value creation include the leader of the operating group on the investment committee. Less-experienced members of the operating group can have consultative arrangements or peer-to-peer relationships with key portfolio company leaders.

Since the main KPIs for operating teams are financial, it is critical that their leaders understand a buyout asset’s business model, financing, and general market dynamics. The operating group should also be involved in the deal during the diligence phase, and participate in the development of the value creation thesis as well as the underwriting process. Upon deal close, the operating team should be as empowered as the deal team to serve as stewards of the asset and resolve issues concerning company operations.

Some funds are also hiring CTOs for their portfolio companies to steer them through large transformations. Similar to the CTO in any organization, they help the organization align on a common vision, translate strategy into concrete initiatives for better performance, and create a system of continuous improvement and growth for the employees. However, when deployed by the PE fund, the CTO also often serves as a bridge between the PE fund and the portfolio company and can serve as a plug-and-play executive to fill short-term gaps in the portfolio company management team. In many instances, the CTO is given signatory, and occasionally broader, functional responsibilities. In addition, their personal incentives can be aligned with the fund’s desired outcomes. For example, funds may tie an element of the CTO’s overall compensation to EBITDA improvement or the success of the transformation.

Bring best-of-breed capabilities to portfolio companies. Buyout managers can bring a range of compelling capabilities to their portfolio companies, especially to smaller and midmarket companies and their internal operating teams. Our conversations with industry stakeholders revealed that buyout managers’ skills can be particularly useful in the following three areas:

- Procurement. Portfolio companies can draw on a buyout manager’s long-established procurement processes, team, and negotiating support. For instance, managers often have prenegotiated rates with suppliers or group purchasing arrangements that portfolio companies can leverage to minimize their own procurement costs and reduce third-party spending.

- Executive talent. They can also capitalize on the diverse and robust network of top talent that buyout managers have likely cultivated over time, including homegrown leaders and ones found through executive search firms (both within and outside the PE industry).

- Partners. Similarly, they can work with the buyout manager’s roster of external experts, business partners, suppliers, and integration advisers to find the best solutions to their emerging business challenges (for instance, gaining access to offshore resources during a carve-out transaction).

Ongoing macroeconomic uncertainty is creating unprecedented times in the PE buyout industry. Managers should use this as an opportunity to redouble their efforts on creating operational improvements in their existing portfolio, as well as new assets. It won’t be easy to adapt and evolve value creation processes and practices, but managers that succeed have an opportunity to close the gap between the current state of value creation and historical returns and outperform their peers.

Source McKinsey. Read the original article here.